Vlad Dzhashi, MD

Are you switching to locum tenens and looking for health insurance to replace your employer sponsored plans?

Great!

Stick around as today I’ll cover how to do EXACTLY this without the risk of brain freeze.

But…FIRST…

Congrats on going “rogue” and starting your locum tenens career! You’ve made a really smart move.

That said, before you rush to celebrate like there’s no tomorrow, here are some points chock-full of reality:

- Who pays for your health and dental insurance when you work locum tenens? ...YOU.

- Are any employee benefits included when you work with locum tenens agencies? ...NOPE.

- Does it mean that you would need to look for them YOURSELF?...HELL YEAH!

So…the bad news, it is YOUR job to make sure you’ve got your safety net before switching to full-time locums.

The good news is that this guide is going to give you actionable steps to make this transition as smooth and painless as possible.

Without further ado…let’s get on it!

Cash “insurance”:

First, you will need some cash. That you don’t spend. Like a cash reserve.

You see, cash is your most important locum tenens insurance and the rule of thumb here is to save enough money to cover at least six months of your basic expenses.

Having that reserve will not only give a piece of mind if your gigs fall through the cracks but you’ll be in a better position to negotiate with hospitals and locums agencies.

Believe me, it’s easier to say NO to a crappy gig with a large chunk of cash in the bank and you’ll have more patience to search for better opportunities.

Now, to make sure your reserve stays intact at all times, “park” it in a separate bank account (saving or yield account) and check it only a few times a year.

Out of sight out of mind…

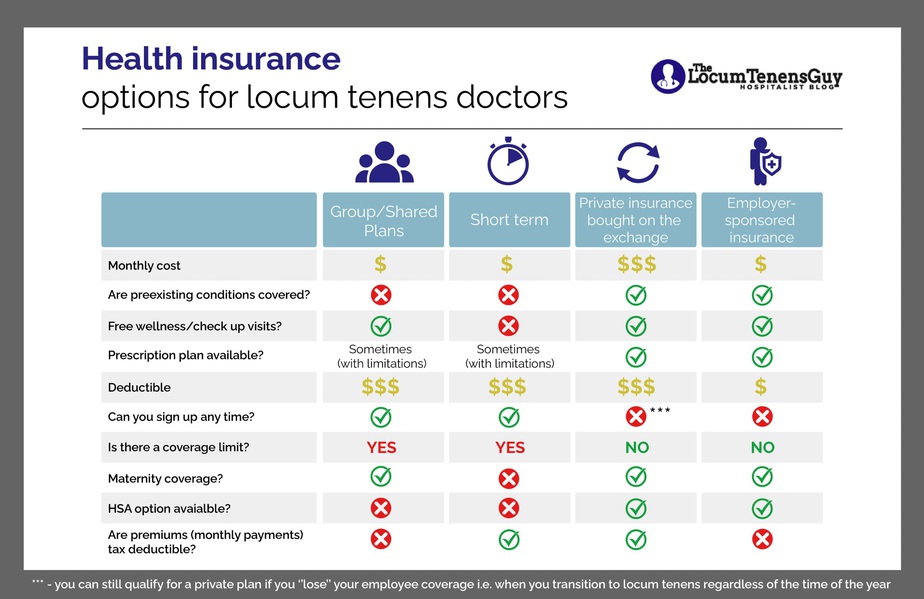

Health insurance for locum tenens physicians:

Now, let’s take a look at your locum tenens health insurance.

If you’ve never shopped for your own insurance before, this WILL BE CONFUSING.

I remember when I was shopping for it, this probably took me days of internet research and multiple phone calls to finally figure this out.

Read on as I’m breaking down health insurance options in more detail.

Health insurance through a family member

If your spouse or partner is employed, check out what it may cost to get on that company’s health insurance plan and this would be your cheapest option in most cases.

Note that you may qualify for this insurance even if you’re not legally married.

COBRA

The Consolidated Omnibus Budget Reconciliation Act (not the snake) guarantees the right to temporarily remain under a former employer’s health insurance plan after you leave your job.

You may stay on COBRA for 18 months, with an option to extend for additional 18 more months.

Compared to the employer sponsored health coverage, you’ll have to pay more out-of-pocket for the insurance since your employer is no longer footing the bill which means your monthly premiums will be HIGH.

And I mean…REALLY high…

For example, when I was switching from my permanent job to locum tenens, COBRA would cost me $2500 a month (!!!)

Whoops…

The main reason for signing up for COBRA despite its cost would be to keep your current treating doctors and avoid other annoyances of switching to the new insurance plan.

Health sharing (Group) insurance plans

Health sharing plans are NOT health insurance. They share health care costs among members of a group. Your premium is deposited into a “potluck” (or rather “pot unluck”) i.e. a community fund.

When you need medical care, the bill’s paid out of that fund. This type of health coverage is typically cheap, sometimes as low as $100/month.

Here’s a list of the major health sharing plans:

- Christian Healthcare Ministries

- Medi-Share

- Samaritan Ministries

- Liberty HealthShare

- United Refuah HealthShare

- MCS Medical Cost Sharing

- Altrua HealthShare

- Freedom HealthShare

- Trinity HealthShare

Most of these companies’ sites have an option to get an instant quote.

Short-term health insurance

Short-term health insurance plans are temporary, year-long, low-premium and high deductible insurance policies that may be renewed for up to three years.

Short-term plans don’t cover things like pre-existing conditions, maternity care, mental health, or prescription drugs.

Caveats: coverage limits and pre-existing conditions

Ok, let’s say you’ve decided to save money and go with cheaper options, i.e. group shared plan or short-term health insurance. Make sure you understand two important caveats.

Coverage Limits

The first one, is that even if you’ve maximized your deductible for the year you may end up having to pay A TON OF MONEY out of your pocket since these policies have an annual or lifetime coverage limit.

The limits may be as low as $100K a year in case of the shared plan or a lifetime limit of $2.5M for short-term insurance policy.

Pre-Existing conditions

The second issue is that you HAVE TO know how your insurance company defines pre-existing conditions as this is where a lot of people got “burned”. Check out this case-study that describes how things may go wrong.

Ok…now when you know all your options, let’s look at how to pick the one for you.

Choosing your health coverage when switching to locum tenens

Here’s a “decision tree” you can use to make a quick choice:

Now if you’re still unsure, just stick to the private insurance as they are regulated by the government and although in most situations costs are high but manageable compared to how much we as doctors make.

Moving on…

Private insurance

The private health insurance is what most locum tenens docs are using (including myself). These plans have no coverage limits or preexisting condition requirements and work similarly to the plan you’ve had as an employee.

Cost of private insurance

The rule of thumb is that your monthly premiums will be at least TWO times MORE and your deductible will be TWO times HIGHER compared to the employer sponsored plans.

Here’s a great resource for the average monthly premium by state and metal tier.

Shopping for the private healthcare insurance

In any state you’ll have at least a few private health insurance to choose from and in the states with lots of insurers you’ll have dozens of options.

There are TWO ways to shop for them: using a broker or using your state’s health exchange site.

Broker may be a good option if you’re purchasing your own plan for the first time and you have some specific questions regarding your personal situation.

You can find brokers here: https://localhelp.healthcare.gov/.

Personally, I used a broker when I bought my shopping for my private insurance for the first time and after I understood the process well, I was purchasing it on the Washington state health exchange.

To use your state’s health exchange you should go to the healthcare.gov and choose your state from the list.

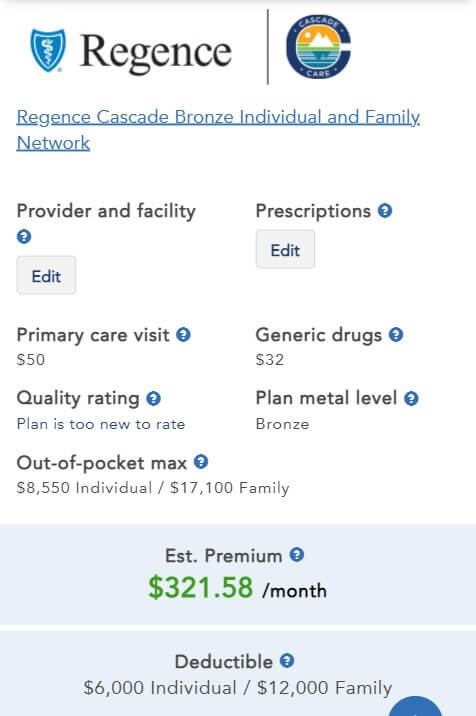

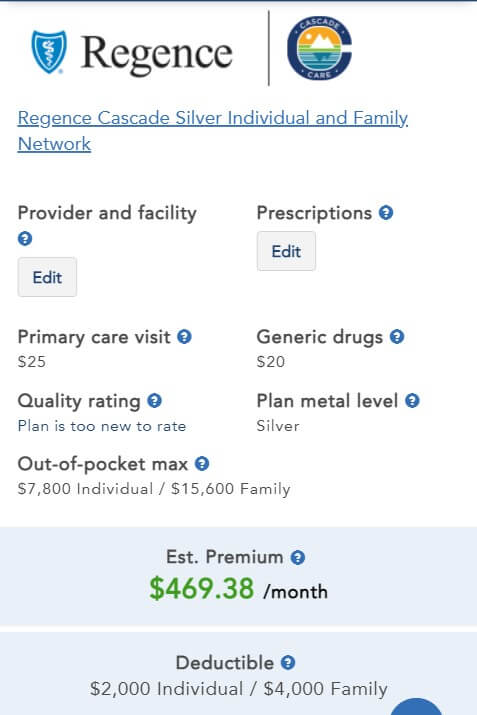

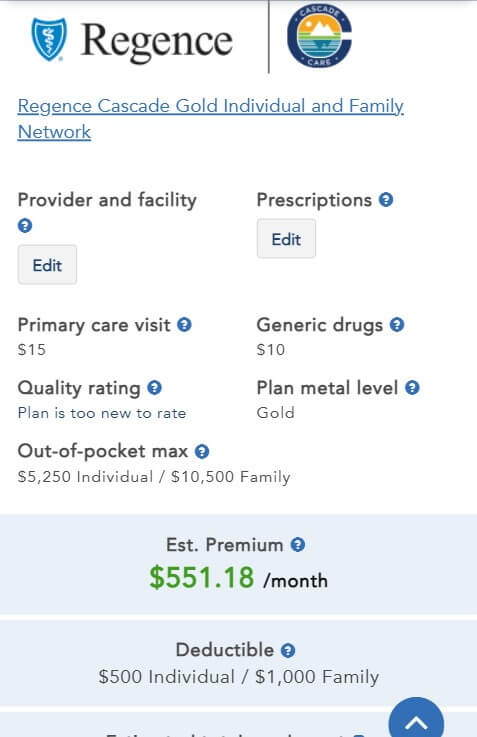

Bronze, Silver and Gold insurance tiers:

Typically you would have a choice of bronze, silver and gold plans (a bag of gold doesn’t come with, sadly).

Here’s an example of WA state:

The lower your premiums are, the higher your deductible is going to be. So for example here your bronze plan has a monthly cost of $321.58 and a deductible of $8,550 whereas the gold plan’s monthly premium is $551.18 and a lower deductible of $5,250.

Gold plan would make sense when you expect to use your insurance frequently, e.g. you need prescriptions, have chronic conditions etc.

HSA or Health Saving Account:

When choosing your locum tenens health insurance, it’s important to decide if you want to go with an HSA plan or not.

Health Saving Account is a savings account that lets you put aside money to pay for your healthcare expenses including your deductible and copays.

Here’s a kicker: HSA gives you a triple tax advantage.

This means you can put pre-tax money into the healthcare fund which grows tax free and if you pay for the healthcare expenses without having to pay tax.

The other good thing, even if you get employer sponsored insurance later on, your HSA fund money would keep growing as an investment.

Personally, I always sign up for HSA if this option is available.

- Jumpstart your Locums Career!

- Sign up for my coaching to access:

- Top Gigs

- Top Pay

- Unique resources

- No stress

- Jumpstart your Locums Career!

- Sign up for my coaching to access:

- Top Gigs

- Top Pay

- Unique resources

- No stress

Vision Insurance

Most vision insurance policies cover your annual eye exam cost and the cost of contacts or prescription eyeglasses. The coverage you get depends on the insurance policy and benefits plan you choose.

Unlike employer-sponsored plans, buying it yourself means you are responsible for the full cost of coverage. Employers typically contribute to the cost, reducing your out-of-pocket costs.

On average, vision insurance packages provided by employers cost the business between $5 and $10 per month for each employee. If you purchase this plan independently, the cost ranges between $5 and $35 per month for an individual.

Dental insurance

Dental coverage will typically fall under two categories.

- General Dental: This includes x-rays, routine cleanings, small fillings, teeth bleaching, and fluoride treatments.

- Major Dental: This policy provides coverage for more extensive treatments, such as dentures, bridges, crowns, and teeth extractions.

The deductible depends on the type of plan you choose. Major dental policies tend to be more expensive than general dental policies.

With an employer-sponsored plan, your employer receives discounts for covering multiple people. The employer may also pay part or all the monthly premiums.

For an individual dental insurance plan, you can expect to pay on average $40 to $50 per month. While this is true, you can find plans that cost as little as $13 per month.

If you opt for major dental, you may pay $140 per month or more.

Offsetting the insurance cost:

As you can see, most if not all insurance options for locum tenens doctors would have a higher premium, higher deductible or if you go with plans with low monthly payments, you would have a bunch of limitations.

Now, the good news is that the IRS lets you take a self-employed health insurance deduction.

NICE! I totally love the IRS now…kinda…

And…you may be able to deduct some medical expenses (doctor visits, hospital fees, and even prescription eyeglasses) that exceed 7.5% of your adjusted gross income.

Now, after we’ve covered a lot of ground for healthcare insurance, let’s talk about other optional health insurance coverage.

Travel Health Insurance for locum tenens

As a locum tenens physician, you will be on the road a lot. If you become ill and need to go to the hospital, you need to ensure you have proper coverage for those situations.

The cost of travel insurance varies based on what you need. But, you can find policies that range in price from $250 to $500.

Some of the factors that will impact your insurance cost include your age, how long you are traveling, and the type of coverage you want. Usually, travel insurance plans cover any medical-related expenses. If you are injured or become ill and require emergency care that may not be covered by your regular health insurance fully, travel insurance may help.

The policy may also cover you being taken to a nearby hospital or even flown home if you become sick or injured. You can purchase travel insurance from a broker or online. The process to purchase it is simple. You can simply:

- Answer questions related to your travel plans

- Receive quotes for coverage

- Select a plan

- Review the coverage and policy

- Purchase the plan

Some plans offer a cancelation period, too, when you can cancel the policy and receive a refund.

If you plan to be traveling for six months or more, having a long-term travel medical insurance plan can be beneficial. With the right travel medical plan, you receive the extra coverage you need while away from home.

You can receive emergency care coverage and coverage for emergency evacuation. When it comes to costs for this insurance, the price is dependent on factors like where you are going.

But, on average, you can expect to pay between $70 and $100.

For longer travel plans, the cost will go up.

If you work with facilities directly, spend lots of time on the road and the travel insurance seems to be too expensive, consider getting a medical evacuation policy.

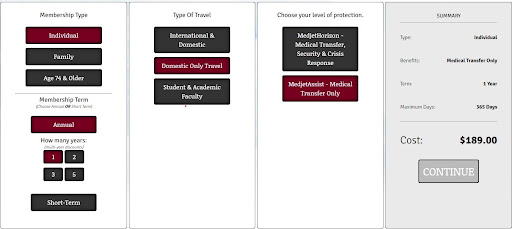

Medical Evacuation policies:

Emergency medical evacuation companies will assist with your transfer in case of the medical emergency.

This policy will cover the cost of your transfer to the hospital close to your home and family, which may run in tens of thousands of dollars if you don’t have this coverage.

As soon as you get to your “in-network” local hospital, your health insurance will cover 100% of your care.

Although this type of coverage will not pay your medical expenses, the medical evacuation plans are MUCH cheaper than a full travel insurance and the cost for these policies are around $200 per year on average.

For locum tenens doctors, this is a smart option and I personally have it.

I’ve been a member with Medjetassist for a few years now. The annual cost is $189 in 2021 and the company has a very good reputation.

Conclusion: health insurance for locum tenens physicians.

Setting up your “safety net” is the most important first step before taking the leap into the locum tenens.

As you can see, you can easily replace your employer sponsored health insurance as long as you pay attention to all the things I covered today.

Now, if health insurance is still too confusing, find a local broker who can help you with choosing the right plan given your situation.

hi Dr Dzhashi,

I’m a Health/life agent licensed in about 14 states and have an unlimited private plan utilizing one of a few nation wide PPO’s (including United Health, Cigna) that seems not to fit into your awesome chart. would you be up for a virtual coffee?