Vlad Dzhashi, MD

If you’re looking to buy your own malpractice insurance for locum tenens work, you may be in for a surprise.

You see, it’s much more than just having vs not having malpractice coverage. There’s lots of important things you need to consider when buying your policy.

And…if you’ve never done it before, this can be pretty confusing.

FEAR NO MORE!

You got LUCKY to stumble upon this post…

Today, you’ll learn what kind of coverage you need for locum tenens, how to save money on it, what to watch out for in your policy to avoid legal troubles and more…

On top of that, I’ll explain everything in PLAIN English, without using any confusing legal jargon, to make sure it’s as clear as it can be.

Let’s jump right in.

Disclaimer: I am not a lawyer nor am I an insurance agent. This post doesn’t provide legal advice or consultation; it is simply for educational purposes. Seek professional opinion.

Occurrence vs Claims-made malpractice insurance

Let’s start with the basics here. There are two kinds of malpractice insurance: claims-made and occurrence.

Claims-made, “Tail” and “Nose”

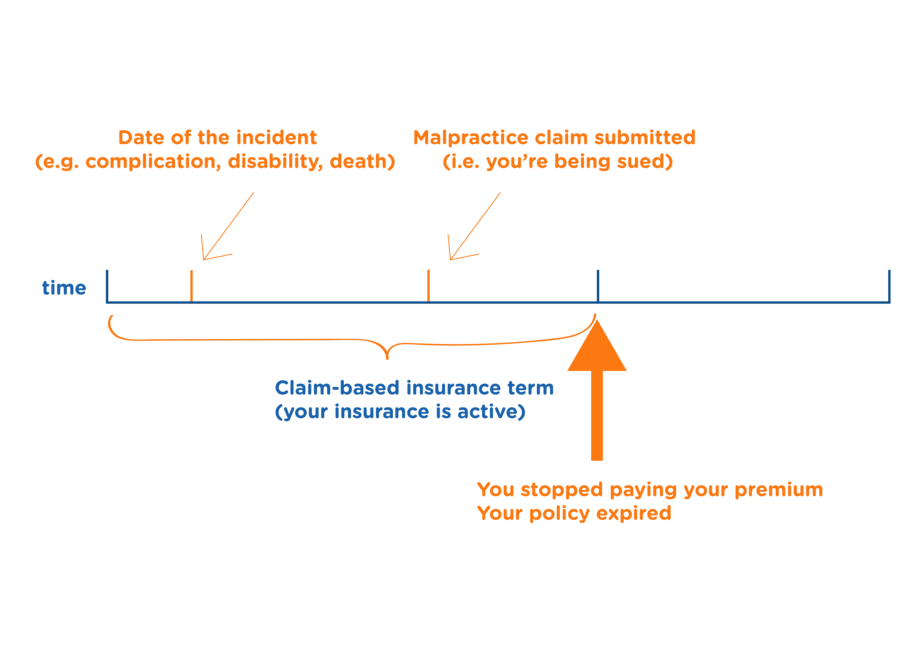

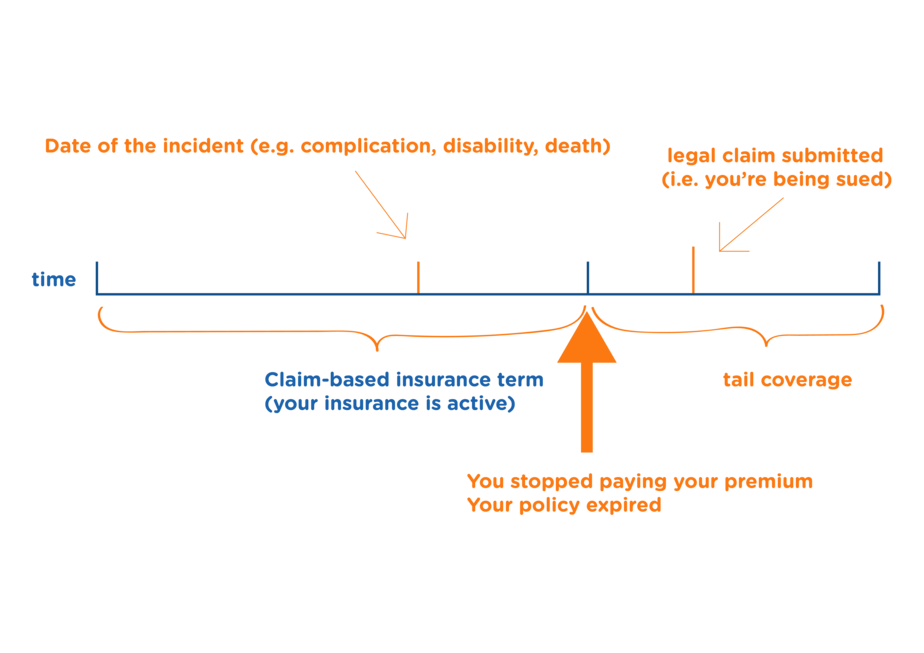

Claims-made policy will cover you only for liability that happened AND was reported (i.e., a claim is filed) while the policy is active (i.e., you are still paying for it).

A little confusing, isn’t it?

Let me give you the visual…

In the above example, your insurance will cover your defense costs and the settlement payout, if it gets to that.

In this case, you are not protected by your medical malpractice policy UNLESS you’ve purchased TAIL coverage from the same or other insurance company.

What is “tail” coverage?

The tail is a supplement that covers events that happened during your policy, even if they were brought up against you after your insurance’s expiration date.

This “upgrade” costs about 200% or more of your last year’s premium.

Ouch…

Another option is to purchase a “NOSE” coverage (also called “prior acts” or “retroactive coverage”). It will cover prior events, and sometimes you can get it cheaper than tail coverage when switching to a new insurance carrier.

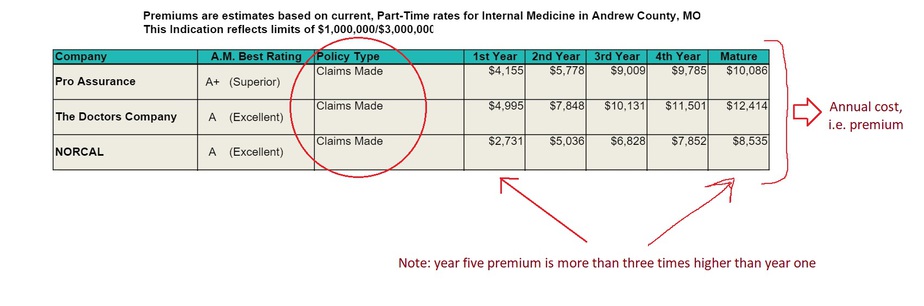

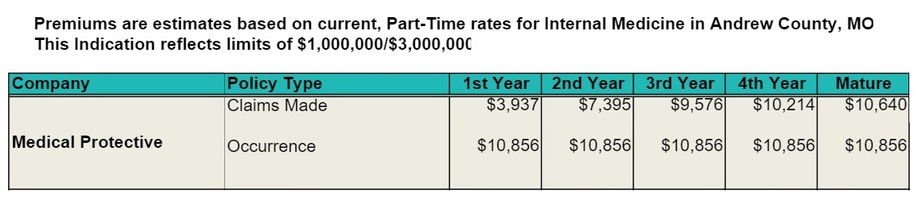

Now, keep in mind that claims-based annual cost goes up over time, reaching its maximum in five years (this is called “maturing”). When your insurance gets to its maturity it would cost at least twice as much as your first year.

Check out the example below which is a quote I got from a broker a couple of years ago…

Occurrence

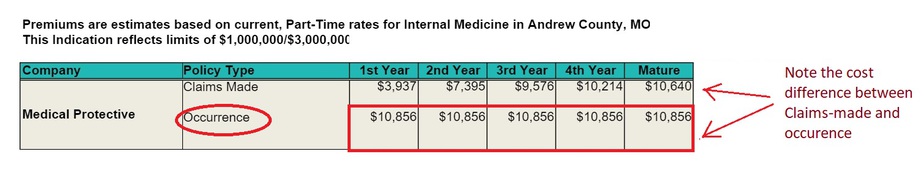

This type of medical malpractice insurance doesn’t require tail no matter when the legal claim is reported as long as the event “occured” during your policy coverage period.

So this one is easy to understand as it works the same way as your car insurance: you pay what you pay without needing to buy tail or nose coverage later on.

And that’s the reason the occurrence policy is more expensive than the claims-made premium, especially if you compare it to the first year or two of the claims-made cost.

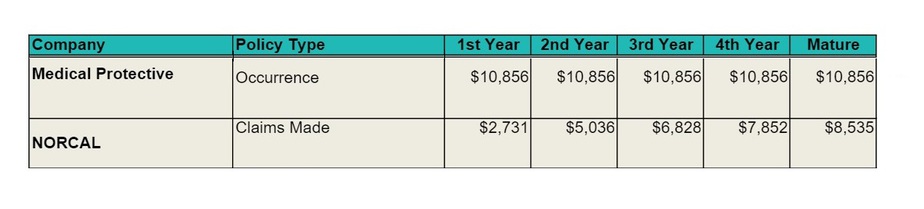

Again, here’s a real life quote:

You can see that a claims-based yearly cost is lower than an occurrence policy in the first couple of years. After that, the difference is minimal, especially if you take the cost of the tail coverage into your calculations.

💡 TLDR:

Claims-based:

- Pros: Cheaper (the tail cost excluded)

- Cons: Each year gets more expensive until year five

- Cons: You need a “tail” or “nose” coverage, which can be 2-4 times of your annual policy cost

Occurrence:

- Pros: NO need to buy “tail” or “nose” coverage.

- Cons: More expensive compared to the claims-based without the tail

- Jumpstart your Locums Career!

- Sign up for my coaching to access:

- Top Gigs

- Top Pay

- Unique resources

- No stress

Malpractice insurance COVERAGE LIMIT

Now, the other big question is how much coverage do you need?

In the locum tenens world, the standard coverage amount has been $1M/3M.

What do these numbers mean?

The first number ($1 million) is for the annual maximum your insurance company will pay for each case and the second number ($3 million) is the total annual amount if you’ve been sued by multiple patients.

Generally speaking, I would stick with the $1M/3M limit as there are potential issues with having too little or too much coverage.

Let me explain…

With the LOWER LIMIT you may be at risk of needing to pay out of your pocket. This may be OK if you practice in state(s) with a very low risk of getting sued (e.g., MN,SD etc…) AND the state has a cap on noneconomic damage (e.g., TX, IN).

Now, you don’t want to have a very HIGH POLICY LIMIT either, as you can become a “scapegoat” if multiple doctors are named in the lawsuit. You don’t want to end up in a situation where your insurance pays out more money than other defendants’ policies, as this may look like it was mostly “your fault.”

The bottom line is: with malpractice coverage limit, you want to be like everybody else.

💡 TLDR:

- $1M/3M is a typical coverage limit for locum tenens

Important malpractice insurance CLAUSES

“The devil is in the details…”

And, dammit, this is so true when dealing with legal mumbo jumbo in the fine print…

As a matter of fact, there are several very important clauses you HAVE TO know about when buying your own locum tenens malpractice coverage.

Defense cost limit:

You want to make sure your policy has NO limit on defense costs, i.e., your lawyer’s fees, expert witnesses fees and other admin expenses.

The trouble here is that these fees can get very costly (hundreds of thousands of dollars at times), and you don’t want to end up paying them out of your pocket.

Deductible:

Believe it or not, some medical malpractice policies have deductibles, which can range between $2,500 and $10,000.

How do they work?

With the indemnity-only (also called “loss-only”) deductible you pay the deductible ONLY if you’ve “lost the case” i.e., the insurance company needs to make a payment to the plaintiff.

With “Indemnity and Expense” you need to pay after the legal case is open regardless of the outcome.

A deductible is not always a bad thing, as it makes your policy cheaper.

“Consent-to-settle” clause

A “consent-to-settle” clause FORCES your insurance company to get YOUR permission before they would settle any case against you.

This is definitely a must-have “perk” as some insurance companies may be tempted to settle the claim even if there’s no fault of yours. This happens if the settlement amount is less than the cost of defending you.

The problem is that this will be reported to the NPDB and will remain in your “biography” forever.

After all, it’s all about money for the malpractice insurance company, but for you, it’s about your reputation.

Hammer clause

The “hammer” clause is something you want to avoid.

It is closely related to the “consent-to settle” clause but may work against you.

Imagine a situation when after the claim is reviewed by the plaintiff and defendant lawyers as well as expert witnesses, your insurance company recommends you to settle the case (i.e. make a payment on your behalf to your former patient or his family).

Despite the advice, you refuse to settle and want to proceed to the jury trial.

Now, let’s say the jury’s decided you are responsible for a higher payout amount than was recommended by your insurance before.

In this case, the “hammer clause” will force YOU to pay the excess, which, of course, can be A LOT of money.

💡 TLDR:

- Make sure your policy has a “consent-to-settle” clause.

- Avoid defense cost limit and “hammer” clauses.

- Check to see if your policy has a deductible, and if so, its amount and the type.

Moving on…

Locum tenens malpractice insurance cost:

I’m sure it’s not a surprise to you, but malpractice insurance can cost a LOT.

What you may have not known, however, is that it can cost up to hundreds of thousands per year.

What…!?

You heard it right…

So pay attention to what AFFECTS your coverage cost, as this may change your approach to where and how you work locum tenens.

Let’s take a look…

Specialty

Some specialties are naturally higher risk, i.e., on average, they get sued more frequently compared to lower risk specialties.

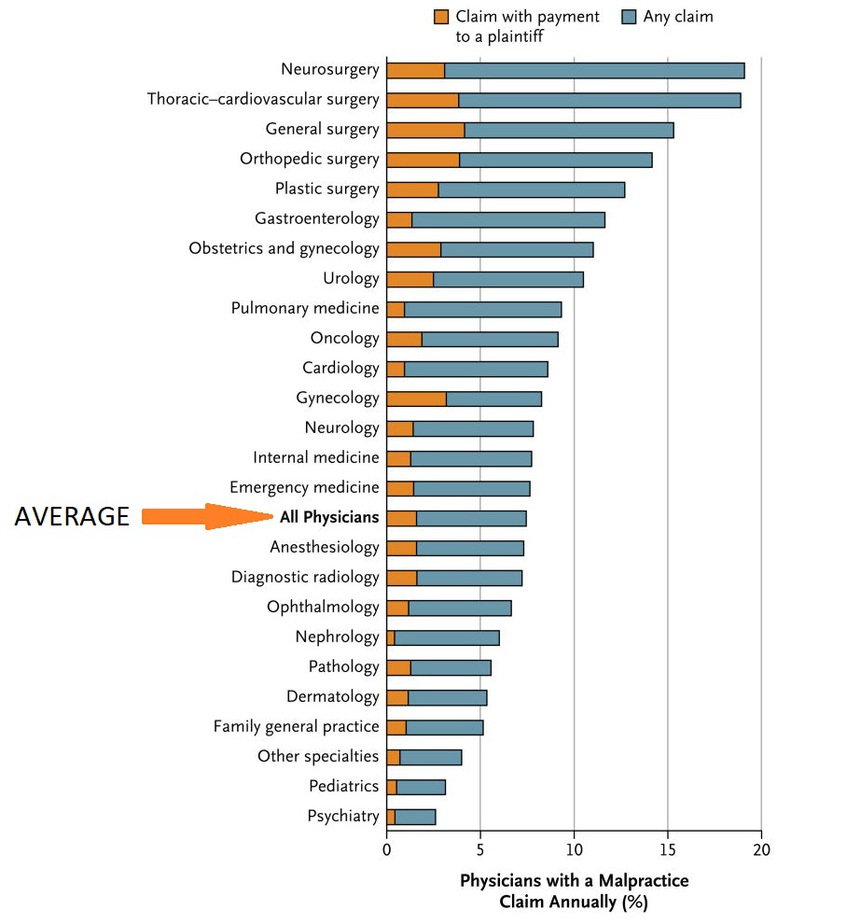

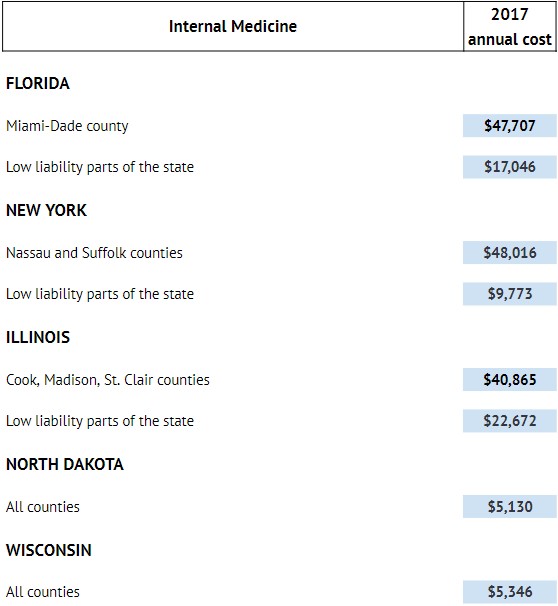

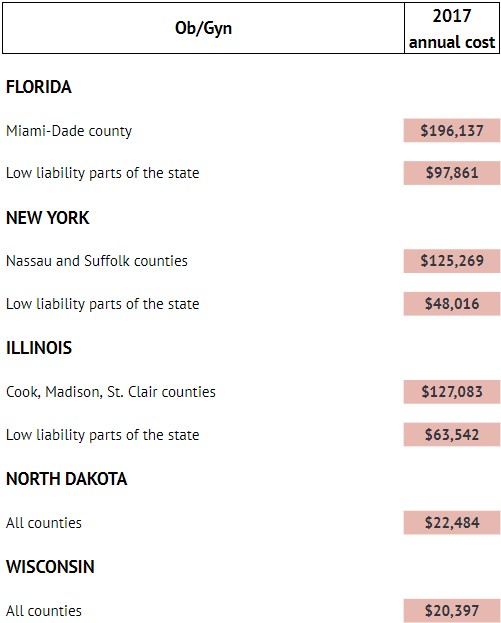

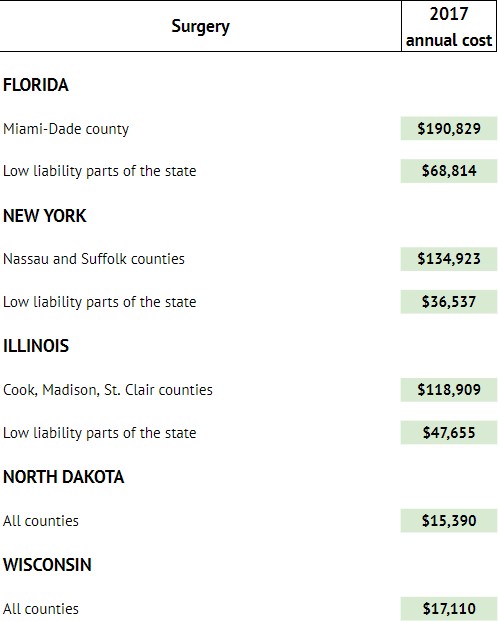

Here’s an interesting data point that was published in NEJM in 2011. They looked at a one-year period to determine what percentage of doctors is being sued based on the specialty.

The other interesting point is that some specialties, like general surgery and Ob/Gyn, are not only getting sued more frequently, but their insurance would make a payment to the plaintiff more often as well.

Where you practice

The cost of your malpractice policy varies a lot based on where you practice as well. This is based on the general risk of being sued as well as the average payouts specific for the area.

What’s interesting is that rates can be different, even within the same state, as more affluent counties tend to sue more and the settlement payouts to the high-earners are larger as well.

When you buy your own locum tenens malpractice coverage, keep in mind you need to let your carrier know if you are going to work in a new location so that they can adjust rates accordingly.

Your cost may go up, go down or remain the same.

If you work across multiple locations with different costs (even if it is within the same state), you’ll pay based on the highest premium.

Look at the example below that gives you a good idea how big of a difference your specialty and geography can make.

Internal Medicine Annual Malpractice Insurance Cost

ObGyn Annual Malpractice Insurance Cost

General Surgery Annual Malpractice Insurance Cost

Besides your specialty and your practice geography, there are other factors that can affect the cost.

Past claims and losses

The more claims you’ve had and the higher the payouts, the more your insurance will cost you.

Coverage limit

Lower limit will mean you’ll get a cheaper policy.

Deductible

If you agree to have a deductible built into your policy, your cost will go down.

How much you work

Your malpractice insurance premium is prorated based on how much you work, so if you work 50% of your average weekly hours for your specialty, you get a 50% discount.

Shopping for your own malpractice coverage

Now, after learning the basics of the locum tenens malpractice insurance, let’s see how we can shop for it like pros.

Where to buy it?

The best way to shop for your own malpractice insurance is to use a broker.

It’s much easier to work with a broker, as you can get quotes from multiple insurance companies and compare the prices.

On top of that, your broker can answer your questions, which is helpful if you’re a newby.

Buying from an insurance carrier is an option too, but I don’t think it is worth it.

You see, you’ll have to request quotes and complete multiple annoying applications to compare the rates between different companies. This will take MORE time and effort on your part without giving you any advantage.

How to find a legit broker?

To find a broker, just google “medical malpractice insurance broker” or use referrals from other physicians.

Here’s a few questions you need to ask before signing up:

- Does the broker specialize in malpractice insurance?

- Does your broker operate in your state of interest?

- Ask for their insurance broker license number and verify online on the official government website (e.g., here’s one for WA state).

- If in doubt, ask for past clients’ contact info to make sure the broker has good reviews.

Decide on what type of policy you want to get

Once you’ve hooked up with a broker, you need to decide if you want to go with a claims-made or occurrence insurance.

The way to do it is to figure out how long you need your coverage for and calculate the cost.

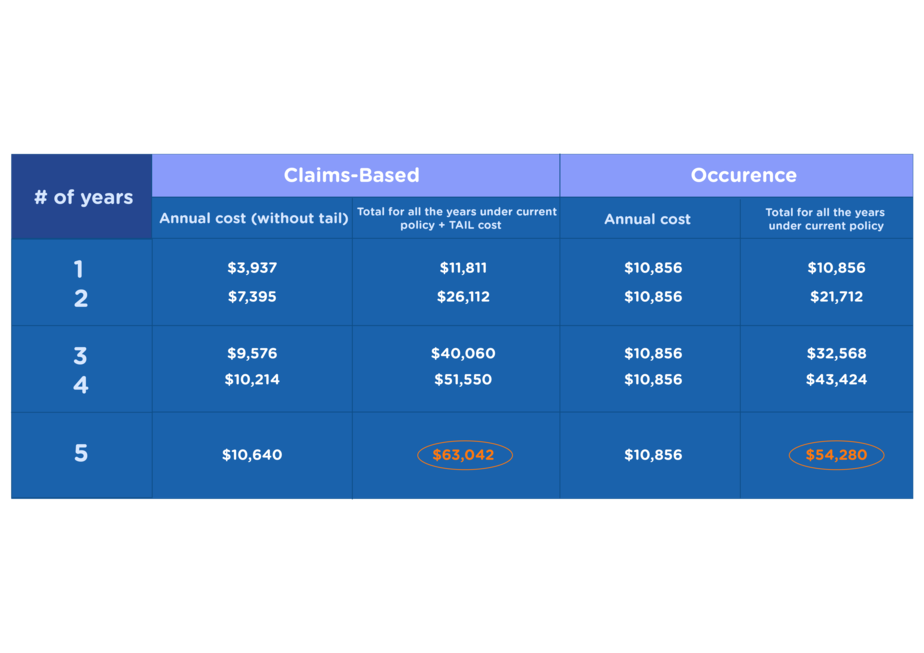

For example, using this quote:

You can calculate how much you’ll end up paying for occurrence vs claims-based options:

So as you can see, with this particular insurance quote, you will be better off purchasing an occurrence policy as you will end up paying less from the get go.

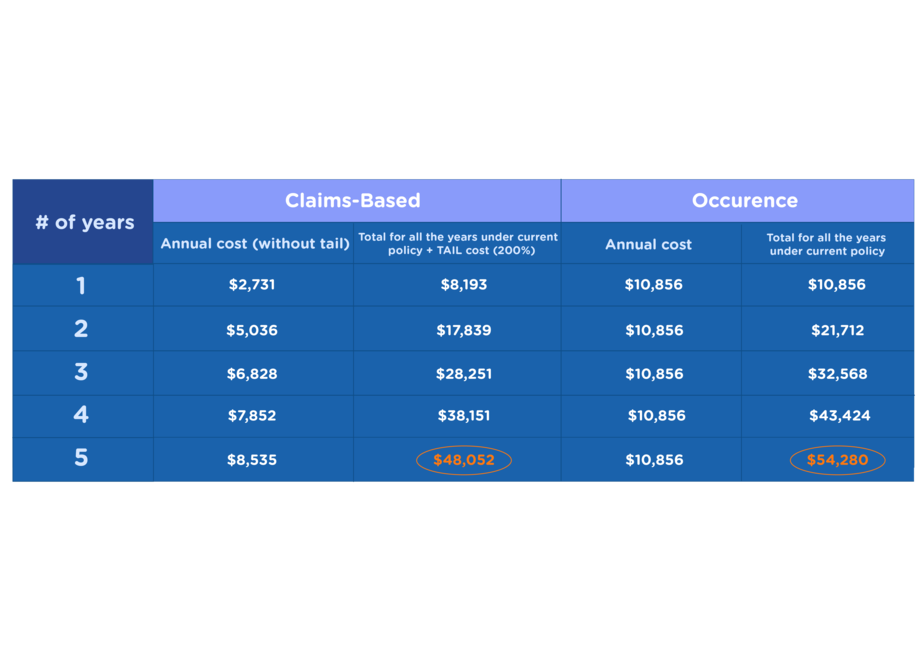

Let’s look at another quote (two different insurers):

As you can see here, it would make sense to get a claims-based policy as it will cost you less.

So…run the numbers before buying to see which options would be better.

Keep in mind that you can switch between claims and occurrence insurance as long as your insurance company provides both options.

Also, you can actually cancel your policy at any point, in which case you can get a prorated amount back, although most carriers will keep at least 25% of the annual cost regardless of when you’ve canceled your policy.

This gives you peace of mind, as you have flexibility if your locum tenens gig dies off or you decide to jump ships and work with a locum tenens company instead.

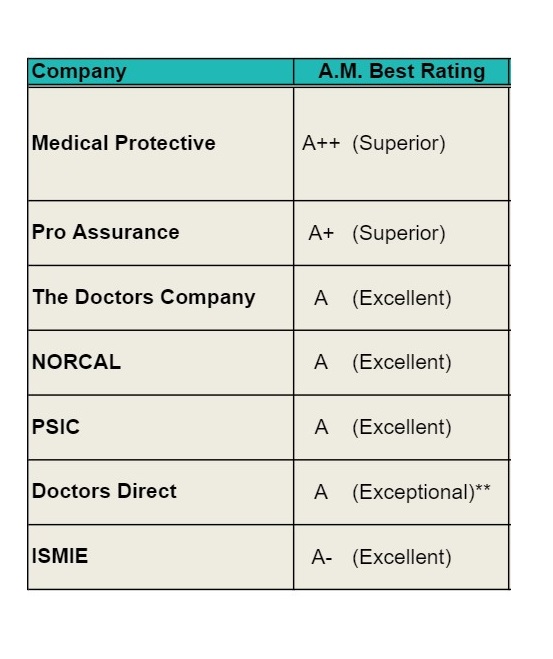

Insurance carrier ratings

If push comes to shove, you want your insurance company to pay the settlement, right?

After all, that’s why you’ve bought the malpractice insurance in the first place.

That’s why you need to check your carrier’s AM best rating. An “A minus” or above is a good indicator the company has a strong financial base.

Five ways to save money on malpractice coverage:

Now, I want to suggest a few ideas on how to save your hard earned money when buying locum tenens malpractice insurance for yourself.

Depending on your specialty and how much you work, this may save you tens of thousands of dollars every year (you are welcome!)

Avoid high liability areas:

The best way to deal with problems is to avoid them in the first place.

Thank you, Captain Obvious!

That’s why picking up locum tenens gigs in state(s) with a better liability situation is the best overall strategy.

If you’ve got coverage already, check with your insurer to see how much you can save by working in a more physician-friendly state. You may be surprised how big of a difference this can make.

Consider a lower limit:

Even though 1M/3M is standard for locum tenens doctors, you CAN go with a lower limit and save money.

$500K/1M or even $250K/$500K may be a good option if you are in the state with a noneconomic damage cap AND your specialty is in a “low-risk” category.

Don’t shy away from policies with deductibles:

If you are ok with having a deductible, you can potentially save tens of thousands every year, as long as you don’t have any past claims.

This makes even more sense if your deductible is low, e.g., $2500 and/or your deductible is indemnity-only [jump link here]

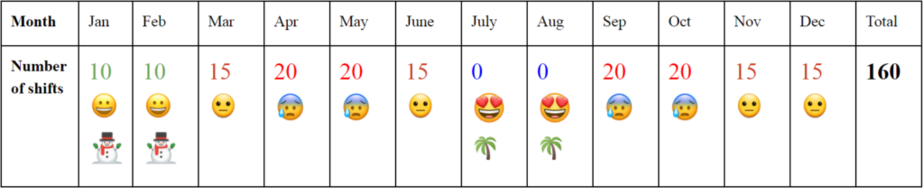

Reduce your hours:

Another approach that can give you cheaper coverage is to cut your work hours to be considered “part-time.”

Of course, you need to crunch the numbers and see if this makes sense for you.

For example, if I were to work part-time only, I would save about $10K a year on the malpractice insurance premium every year. But…I would “lose” $150K-200K by reducing my work hours.

So for me, as an internal medicine hospitalist practicing in WA state, switching to part time just to save money on malpractice insurance would be nonsense.

On the other hand, this may make sense if your malpractice premiums are sky high (e.g., you’re an ObGyn physician working in affluent Florida counties).

“Clean” background discount:

Some insurers offer a discount (10-15%) if you have no malpractice history, so check with your broker if this can be applied to your policy.

What if your policy is TOO cheap?

Now, we’ve talked about how to make your malpractice coverage cheaper, but what if some insurers’ quotes seem TOO LOW to be true?

If this happens, my suggestion is to ask your broker why.

- Does the policy have one or more of the “sneaky” clauses I talked about earlier?

- Is there a high deductible or defense cost limit?

- Does the insurance company have a low AM Best Rating? Or maybe it’s not rated at all?

This is where your broker’s knowledge and expertise can help you to weed out “bad” players from the good ones.

That said, if there’s a potential risk, I would always prefer a more reliable option, even if it’s more pricey.

💡 TLDR:

- Use a specialized malpractice insurance broker to get quotes from multiple companies.

- Figure out how long you need the coverage for and calculate if claims-based or occurrence policy makes more sense.

- Pay attention to the insurance company “AM Best Rating”, A- or higher means the company has a good financial base.

- Save on malpractice coverage: avoid high-risk areas, consider lower policy limits and policies with deductibles, work part-time and ask for a “clean” background discount.

- If there’s a big difference between different quotes, ask your broker for an explanation.

The Anatomy of Malpractice Certificate Of Insurance (COI)

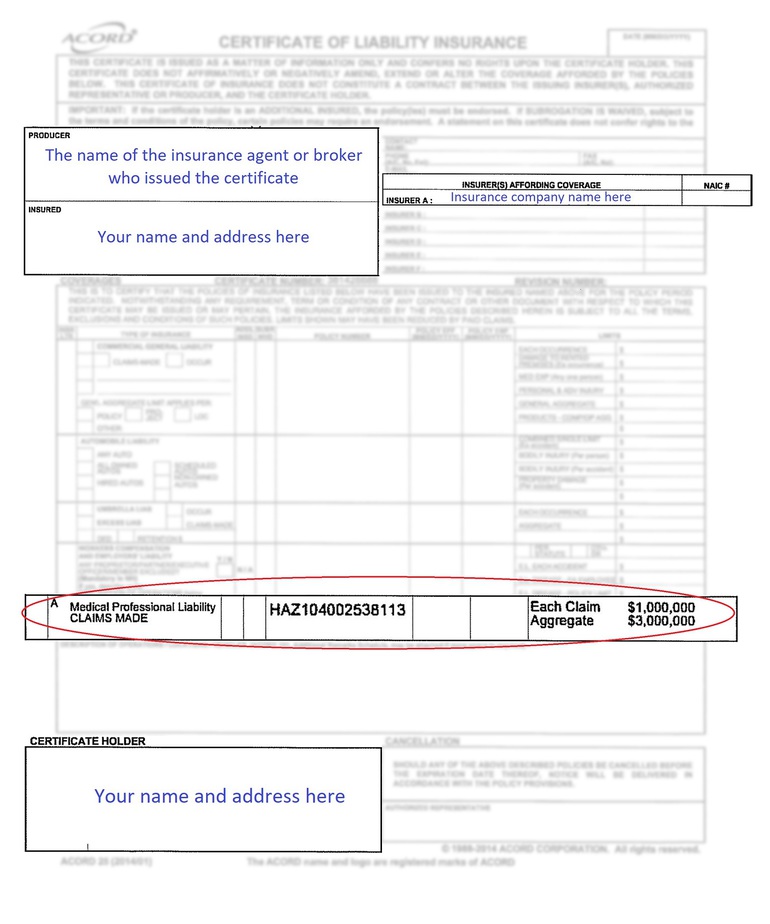

Now, after you’ve paid your “dues,” your next step is to get a copy of the Certificate Of Insurance (COI).

COI is a document that confirms your insurance status. Think about it as your insurance policy ID.

Here’s what it would look like:

Once you’ve received your certificate, pay attention to the spots I highlighted for you on the image, and make sure your name, address, policy limit and insurance type are all correct.

Since you typically need your previous COI’s when applying for hospital credentialing, I suggest you scan it and store it on cloud storage and your laptop.

Moving on…

The little big FYI: how NOT to get cancelled...

No, I am not talking about “cancel culture” here, I am talking about legit and legal reasons why your malpractice insurance carrier will revoke your coverage.

These things may seem to be obvious, but it is still worth mentioning since losing your coverage is a HUGE deal:

- If the physician DIDN’T disclose anticipated or pending claims before signing up for a new policy.

- If the physician was under the influence of intoxicants or narcotics while treating a patient.

- If the treatment provided by physician was experimental, or was part of the research or trial.

Conclusion: Knowledge is power!

Phew…

Today, I’ve given you a crash course on buying your own malpractice insurance.

Now you know more than 99% of US doctors about this extremely important topic, which, if not approached with caution, can mess up your career and finances.

As always, I am on the lookout for your questions, so leave your comments below and I’ll respond ASAP.

- Jumpstart your Locums Career!

- Sign up for my coaching to access:

- Top Gigs

- Top Pay

- Unique resources

- No stress