Vlad Dzhashi, MD

Paying taxes is an inevitable evil.

On top of that, taxes are confusing!

But…I’m absolutely convinced that every locum tenens guy and gal needs to grasp the basics. This is especially important for “newbies” who are either graduating from residency/fellowship or switching from full-time employment.

What was it?

You don’t feel like reading about locum tenens tax deductions?

Hmm…how about MAKING MONEY? Everybody LOVES reading about how to earn more.

Now…using tax deductions, reducing the tax burden, and saving on taxes is THE SAME as making more money since in both cases you’ve got more cash left in your pockets.

Ahh…now I see you got interested…

Let’s dive in and learn in nauseating details 100% legal ways to keep more $$ for ourselves!

Disclaimer: Always discuss the specifics of your situation with a CPA and consider signing up for a tax review and tax tips with an experienced tax professional providing custom-tailored services to the locum tenens doctors.

Physician locum tenens taxes vs W2 taxes:

The first thing first, If you are new to locum tenens work you must know that now you are an independent contractor which means you are self-employed and your locum tenens taxes will be different from W-2 taxes that you used to file.

1 – Nobody withdraws your income tax from your paycheck anymore so now it is YOUR responsibility to make regular tax payments to the IRS (federal tax, self-employment tax, and state tax).

2 – Your tax return will look different: you will have to pay taxes four times a year in contrast to once at the end of the year.

3 – Now you can deduct business expenses, i.e. the thing that cost you money but are required to conduct your “business” as a locum tenens physician.

This will be the case REGARDLESS of whether you work using a staffing agency or work directly with the hospital as long as you are paid as a 1099 physician.

HOME OFFICE locum doctor tax deductions

What is a home office in the IRS' eyes?

A room or an area of your home that you use ONLY for your “business” activities on a REGULAR BASIS: e.g. charting, communicating with locum tenens agencies, applying for new licenses, printing and scanning documents, bookkeeping etc.

Your home office could be a whole room or a part of it (e.g. you have a bedroom that you use as such but you also have a desk with a printer).

What expenses can you deduct?

A portion of mortgage interest, insurance, maintenance, which is based on the square footage of your home office area, are allowable in locum doctor tax deductions

And…great news if you are renting as you can also use this deduction!

Can I deduct rent if I work away from home?

Yes! As a locum tenens doctor, you may work away most of the time, but the good news is YOU CAN deduct a part of your rent proportional to the area you are using as your home office deduction.

Non-deductible:

Room or area that you use for business activities AND it serves as a media room or bedroom at times (even if occasionally).

PERSONAL CAR tax deductions for locums doctors

If you use your personal (i.e. not rented) car to travel to locum tenens assignments, your tax advantage will usually come in one of the two forms:

“All-inclusive” IRS mileage rate

The most common option is to use the “all-inclusive” IRS mileage rate, which changes every year and it is $0.575 per mile in 2020.

So, for example, you decided to drive to the neighboring state instead of flying and covered 500 miles both ways. Also, while working away from home you drove 10 miles every day for 15 days to get from the hotel to the hospital and back.

Your total mileage would equal: 500 + 10 * 15 (10 miles daily for 15 days) = 650 miles

To calculate the money value you need to multiply total mileage by IRS rate, or 650 miles x $0.575 which equals $373.75.

Now, when you work with an agency this amount will be added to your paycheck and will be tax-free.

If you work with the hospital directly as an independent contractor, this amount is allowable as tax deductions for doctors.

Actual car expenses

A second option is to track ACTUAL car-related expenses and write them off: gas, maintenance, insurance, repair costs, etc.

It’s much more cumbersome and may not lead to any extra tax savings compared to the first approach.

Non-deductible:

Commuting is NOT deductible, i.e. your driving between your home and clinic/hospital that you work at on a regular basis.

Locum tax deductions for TRAVEL EXPENSES

What locum tenens travel expenses are considered to be deductible ?

Any travel expenses that you have while spending a night(s) away from home for an assignment that is temporary (will last less than a year).

What travel expenses CAN locum tenens physician deduct?

If you are paying for your travel expenses out of pocket you can deduct following:

- Airfare including baggage fees

- Rental car or Personal car expenses (if driving your own car)

- Gas

- Hotel/Accommodation

- Parking and tolls

- Meals (please see detailed explanation below)

If your expenses are REIMBURSED or PAID by the agency, the only travel deduction you can claim is meals.

Non-deductible:

Parking, toll fees, gas expenses while commuting (i.e. not spending night away from home working on a temporary assignment)

MEALS: doctors’ tax deductions for food

Meals are deductible as long as you travel to your locum tenens assignment and not just commuting.

Any travel expenses that you have while spending a night(s) away from home for an assignment that is temporary (will last less than a year).

You've got two options here:

- 1 - You can deduct 50% of actual meal costs (you MUST track actual expenses)

- OR

- 2 - You can use a standard IRS per-diem meal rate. In this case you DON’T have to keep track of your expenses.

Are per diem meals 100% deductible?

Per diem meals are deductible at 50%, and is the standard method of tracking meal expenses on the road, as it’s easy and effective. To prove the per diem days you claim were in fact days you were contracted to work, it’s a very good idea to save your assignment contracts.

Non-deductible:

Any meals you paid for at the hospital/clinic within commutable distance from your home (i.e. you didn’t have to stay at a hotel and drove back home after work).

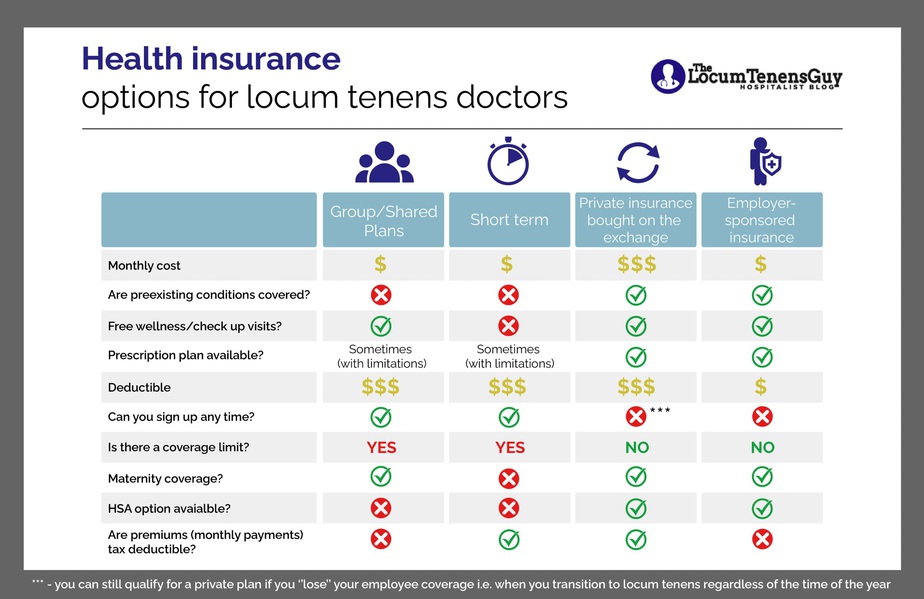

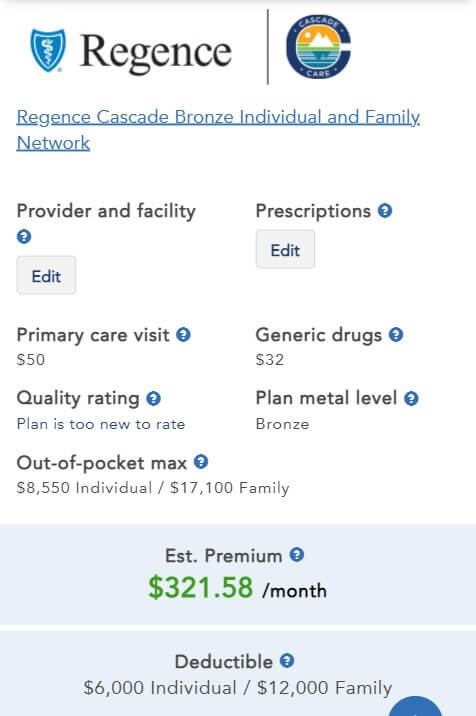

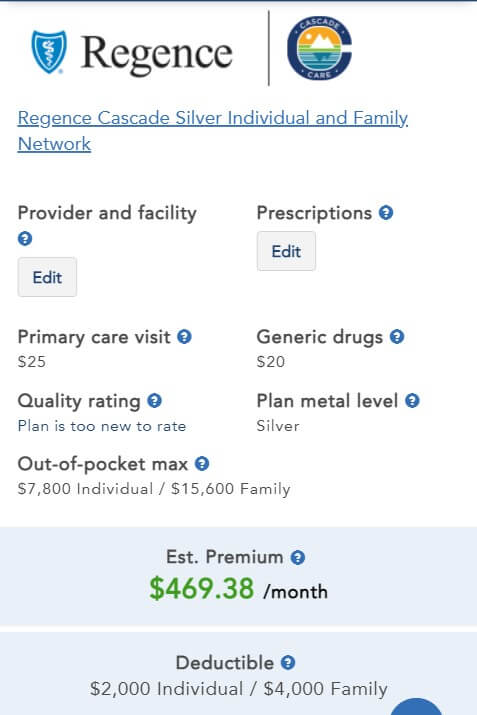

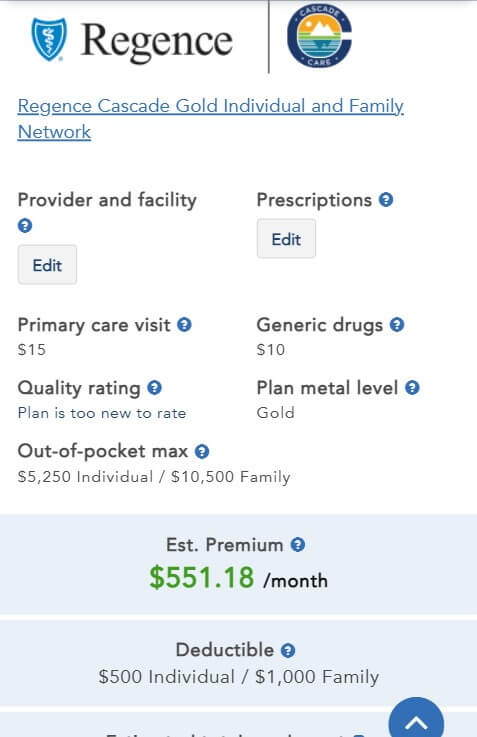

HEALTH INSURANCE locum tenens physician tax deductions

What health insurance expenses can locum tenens doctor deduct?

Health insurance premiums (i.e. your monthly payments including dental insurance) and HSA contributions are tax-deductible.

Non-deductible:

Healthcare expenses, e.g. doctor or hospital fees, medication costs unless paid using the HSA fund.

TRAINING/CME tax deduction

Airfare, hotel and course fees are deductible as long as they are required to attend your seminar.

All other educational expenses are deductible as well including: books, journal subscriptions, ACLS/BLS certification, board exam preparation course etc.

Non-deductible:

If a CME conference is just an excuse to have an extended vacation, GOOD TRY, but the personal portion of the trip’s cost IS NOT deductible.

UNIFORM: are scrubs tax deductible?

Only clothing specific to the job (i.e. scrubs, labcoat) will be deductible.

Non-deductible:

Anything that can be seen as “street” clothing is NOT deductible.

Damn it…no “cheap” Gucci shoes for me!!!

CELL PHONE locum tenens tax deductions

Estimate how much of your usage is business-related and deduct the respective portion. I typically deduct 50%.

You can deduct 100% of your phone expenses ONLY if you’ve more than one phone and use it EXCLUSIVELY for your locum tenens related communication.

You can also deduct the cost of the phone itself, again, keeping in mind how much of its use is personal vs business.

Other deductible locum expenses

- Professional fees: including CPA fees, legal fees (e.g. contract review expenses)

- Office Supplies: paper, ink, printer, laptop

- Licensing: including fees, DEA, fingerprinting services etc.

- Healthcare expenses: but only if they exceed 7.5% of your adjusted gross income.

- Retirement plan contribution: e.g. SEP-IRA or other retirement accounts.

How much can a locum tenens physician write off the taxes?

A lot of doctors want to know how much money they can deduct from their 1099 taxable income. In my experience, if you travel away from home and work locum tenens full time, you will be looking at anywhere between $5000 to $15,000.

So, if you are in the 30% tax brackets, you will save $5000 * 30%, or $1500 per year on the lower end and $15000*(keep in mind these are very rough calculations).

Legal entity and tax deductions

Now, I cannot give advice on forming a legal entity like an LLC or C-Corp this is why it’s a good idea to get professional tax advice.

The last thing I wanted to mention is that you can claim all the 1099 deductions for physicians that I mentioned even without setting up an LLC or Corporation.

Keeping track of your expenses

Once you learn what those deductible expenses are, the next big thing is to make sure you keep track of ALL of them.

This was something I was struggling with initially. You see, when there are so many different items to deduct it’s really easy to forget about them which means you are literally LOSING money. So I used to waste a lot of time going through all the transactions for that tax season.

That’s why you HAVE to use one of the approaches that I describe in my post on organizing the locum tenens life whether you use debit or credit card to pay your business expenses.

And, make sure to download the spreadsheet below to make your life easier.

BONUS: 1099 expense tracker

DON’T FORGET!

Don’t forget to add your allowable locum tenens tax deductions as expenses in my locum tax calculator when estimating how much tax you’ll likely pay.

Key takeaways on physician independent contractor tax deductions

As you can see as a locum tenens/independent contractor physician you can deduct a lot of expenses. By now you should have a pretty good idea of what these things are and how to keep records of ALL your expenses.